{kind=link}

Are Atlanta mortgage rates headed back to the 3% era anytime soon?

Short answer: probably not this year.

Rates in Metro Atlanta sit around 6.5% to 7.0% in early 2025, and economists expect real relief only if the Federal Reserve (the Fed) starts cutting rates in late 2025 or 2026.

That timing is uncertain, and week-to-week moves will matter.

This post lays out the likely rate paths, how those swings reshuffle monthly payments and neighborhood affordability in Atlanta, and the practical steps buyers should take to be ready.

Key 2024–2025 Atlanta Mortgage Rate Projections Buyers Must Know

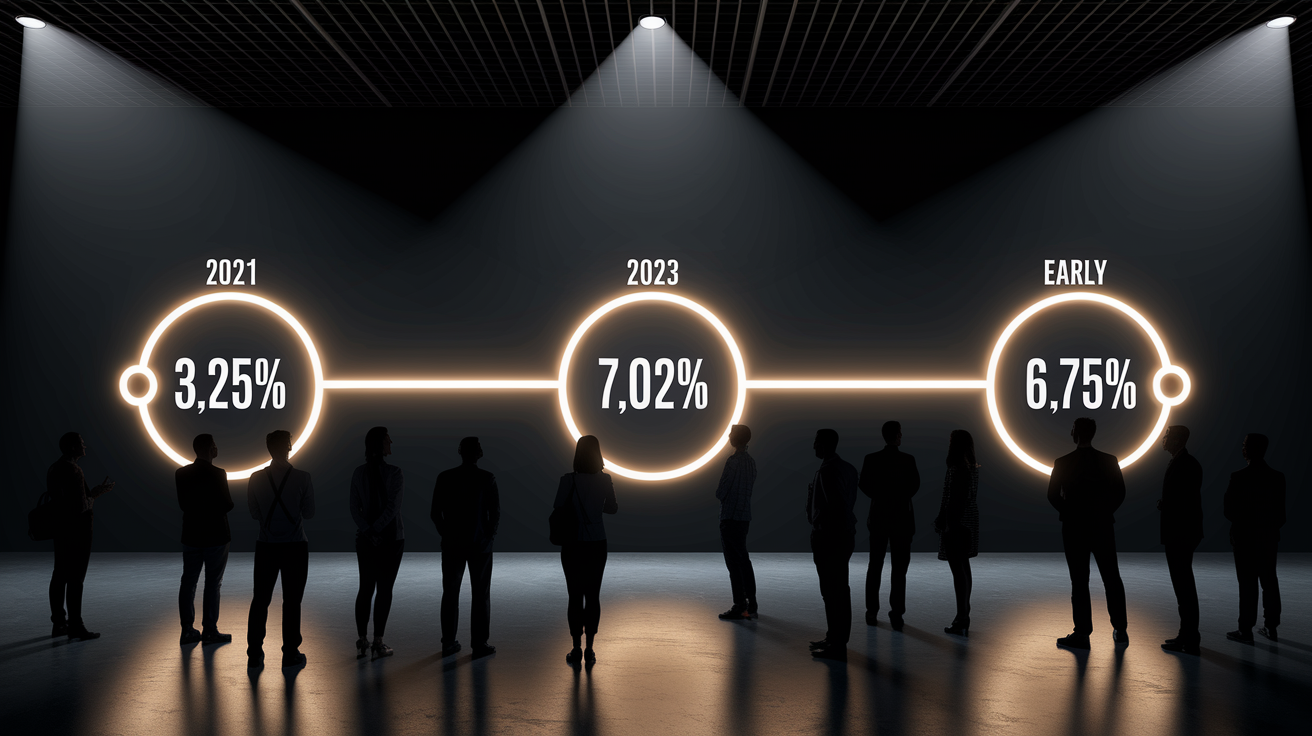

Mortgage rates across Metro Atlanta are sitting around 6.5% to 7.0% in early 2025. That’s a bit below the 7.0% peak we saw in 2023. Most lenders and economists think rates will ease up later in 2025 or into 2026 if the Federal Reserve shifts toward cuts, but nobody’s certain about timing. The historical path is pretty dramatic: rates were near 3.25% in 2021, jumped to 7.0% by 2023, and have only softened modestly to around 6.75% by early 2025. You should expect continued volatility through the year as inflation data and Fed signals drive week-to-week movement.

For Atlanta buyers, these projections matter because North Metro Atlanta’s low inventory and steady population growth mean even modest rate drops can spark bidding wars and push prices higher. Buyer demand dropped sharply in 2023 when rates peaked, rebounded slightly in 2024, and remains well below the multiple-offer frenzy of 2021–2022. If rates fall in late 2025, pent-up demand is likely to flood the market, reducing negotiation leverage and shortening time on market. Buyers who are prepared with pre-approval and clear budgets will have an edge over those waiting until the surge begins.

Affordability shifts happen fast when rates move. A one-percent rate change alters monthly payments by hundreds of dollars, changing which neighborhoods and home sizes fit inside your budget. Understanding the trajectory and preparing for both “rates stay high” and “rates fall faster than expected” scenarios gives you flexibility to act when the market window opens.

Top rate forecasts you should monitor:

- Potential late-2025 or early-2026 Fed easing if inflation cools further

- Movement in 10-year Treasury yields, which anchor mortgage pricing

- Local lender predictions based on Atlanta-specific demand and inventory signals

- Any Fed policy surprises that accelerate or delay the rate-easing cycle

How Atlanta Mortgage Rate Trends Affect Affordability and Monthly Payments

Each percentage point change in your mortgage rate rewrites your monthly budget. On a $750,000 loan (principal and interest only, excluding taxes, insurance, or HOA fees), a 3.5% rate costs you $3,368 per month. At 6.0%, that same loan jumps to $4,497, an increase of $1,129 every month. Push the rate to 7.0% and you’re paying $4,990, another $493 more than the 6.0% scenario. The full swing from 3.5% to 7.0% adds $1,622 to your monthly payment, or nearly $19,500 per year. Those numbers shrink your purchasing power and push some buyers into smaller homes, different neighborhoods, or extended timelines.

Rate sensitivity hits first-time buyers and move-up buyers differently. First-time buyers often stretch to the top of their approved budget, so even a half-point rate increase can knock out their target home or force them to drop features like extra square footage or a preferred school district. Move-up buyers already own a home, which usually means they’re carrying a low-rate mortgage from 2020 or 2021. Trading a 3.0% rate for a 6.5% rate feels expensive, even when the new home is larger or better located. That reluctance keeps inventory tight and prices stable, because fewer sellers list when giving up their low rate means accepting a much higher payment on their next purchase.

| Rate % | Monthly Payment (P&I only, $750k loan) | Difference vs Prior Rate |

|---|---|---|

| 3.5% | $3,368 | — |

| 6.0% | $4,497 | +$1,129 |

| 7.0% | $4,990 | +$493 |

Understanding how rate changes reshape your monthly payment helps you decide whether to buy now, wait for lower rates, or adjust your home search to fit a higher-rate reality. The difference between a 6.0% and 7.0% mortgage isn’t just $493 a month. It’s the margin that determines whether you can afford the home you want or need to settle for something smaller.

Key Factors Driving Projected Atlanta Mortgage Rate Trends

Federal Reserve policy sits at the center of every mortgage rate projection. When the Fed raises its benchmark rate to combat inflation, mortgage rates climb. When the Fed signals cuts (usually after inflation cools or economic growth slows), mortgage rates tend to fall, though the timing and size of those drops depend on how financial markets interpret the Fed’s next moves. Late 2025 or early 2026 could bring rate relief if inflation continues trending down and the Fed shifts toward easing. But any surprise inflation spike or strong jobs report can delay cuts and keep rates elevated longer than buyers expect.

Inflation trajectory matters because mortgage investors price loans based on expectations for future purchasing power. If inflation stays high, lenders demand higher yields to offset the risk that dollars repaid years from now will buy less. Treasury bond yields, especially the 10-year, move in tandem with inflation expectations and directly influence mortgage pricing. When the 10-year Treasury yield rises, mortgage rates follow. When it falls, rates ease. Atlanta buyers should watch national inflation reports and Fed meeting statements, because those indicators telegraph whether the late-2025 easing scenario remains on track or gets pushed into 2026.

Local Atlanta dynamics amplify or dampen national rate trends. Metro Atlanta’s population growth continues to outpace new housing permits, creating persistent supply pressure that keeps prices elevated even when rates rise and buyer demand softens. Buyer sentiment cycles matter too. When rates spiked in 2023, demand dropped sharply, but inventory stayed low because sellers with 3% to 4% mortgages chose not to move. That created a standoff. Fewer buyers, but also fewer homes for sale. Which stabilized prices and prevented the deep corrections seen in other markets.

Most influential rate drivers specific to Metro Atlanta:

- Local demand growth: Atlanta’s job market and in-migration keep baseline housing demand high, even when rates discourage marginal buyers.

- Supply constraints: New construction and listing inventory haven’t caught up to population growth, reducing downward pressure on prices when rates rise.

- Buyer sentiment cycles: After sharp 2023 demand drops, partial 2024 rebounds showed that Atlanta buyers return quickly when rate or price conditions improve even slightly.

Local Atlanta Housing Market Dynamics That Shape Mortgage Rate Impact

North Metro Atlanta’s inventory shortage didn’t start with high rates. It deepened because of them. Homeowners who locked in 3% to 4% mortgages in 2020 and 2021 are understandably reluctant to sell and trade up into a 6.5% or 7.0% loan. That “rate lock-in” effect removes a huge slice of potential inventory from the market, especially among move-up sellers who would normally list every few years. In Alpharetta and Milton, the result is fewer homes for sale, longer time on market in higher price tiers where rate sensitivity is strongest, and stable or even rising prices in entry-level and mid-range segments where limited supply keeps competition alive.

Rental market spillover adds another layer. Rental vacancies in Metro Atlanta are up nearly 2% year over year and sit above the national average, which can increase the pool of renters ready to buy and push some landlords to sell when vacancies rise. At the same time, new construction continues. Atlanta issued 74 new permits per 100,000 residents in May 2023, well above the national average of 43 per 100,000. But permit growth still lags population growth. New builds help, but they don’t fully offset the inventory gap, and many new-construction buyers are first-timers or downsizers who aren’t selling an existing home, so new builds don’t always free up resale inventory.

Rate changes hit different price segments unevenly. Higher-priced homes in Alpharetta, Milton, and Buckhead see more negotiation and longer listing times when rates rise, because the absolute dollar increase in monthly payments is larger and buyers in those tiers often have more flexibility to wait. Entry-level and mid-range homes in Marietta, Smyrna, and parts of Decatur tend to hold their value better during rate spikes because low inventory and steady first-time buyer demand keep competition alive. If you’re targeting a home above $600,000, expect more room to negotiate in a high-rate environment. Below $400,000? Expect faster sales and less wiggle room on price.

Which Atlanta price segments are most rate-sensitive:

- $700,000 and above: longer days on market, more price cuts, turnkey condition becomes critical

- $400,000 to $700,000: moderate sensitivity, stable in strong school zones and near job centers

- Below $400,000: least sensitive, low inventory keeps competition high even when rates rise

- New construction: appeals to buyers prioritizing move-in-ready and modern features, less rate-sensitive than older resale inventory

For more detail on how interest rates influence Atlanta pricing and supply across neighborhoods, see How Interest Rates Are Shaping The House Market in Atlanta.

Historical Atlanta Mortgage Rate Trends and What They Signal for 2025–2026

Atlanta’s mortgage rate path over the past four years shows how fast affordability can shift. Rates sat near 3.25% in 2021, fueling a buying frenzy with multiple offers, waived inspections, and homes selling in days. By 2023, rates had climbed to 7.0%, demand dropped sharply, and the market cooled. Early 2025 brought a slight decline to around 6.75%, but that modest easing hasn’t reignited the 2021–2022 intensity. Buyers have more time to think, inspect, and negotiate. But inventory remains tight because so many homeowners are still holding onto their sub-4% mortgages.

The 2021–2022 low-rate environment created a once-in-a-generation window for buyers, but it also set up the current inventory crunch. Sellers who bought or refinanced during that period have little financial incentive to move unless life circumstances force it. Job relocation, growing family, downsizing. That reduces turnover and keeps available inventory below historical norms. In 2023, when rates peaked, demand fell but so did listings, preventing the price drops that usually follow demand declines. In 2024, buyer demand rebounded slightly, but not enough to return to 2021–2022 levels, and inventory stayed constrained.

| Year | Average Rate |

|---|---|

| 2021 | ~3.25% |

| 2022 | Rising (mid-year spike began) |

| 2023 | ~7.0% (peak) |

| Early 2025 | ~6.75% |

These cycles teach us that rate changes drive behavior more than absolute rate levels. A drop from 7.0% to 6.0% feels like a huge relief and pulls hesitant buyers off the sidelines, even though 6.0% is still double the 2021 rate. If rates fall in late 2025 or 2026, expect pent-up demand to flood the market, shrink inventory further, and push prices higher. Past cycles also show that waiting for the “perfect” rate can backfire. By the time rates drop, competition returns and prices rise, erasing the monthly payment savings you were hoping to capture.

Actionable Buyer Strategies for Navigating Projected Atlanta Mortgage Rate Trends

The decision to buy now or wait hinges on your timeline, your budget flexibility, and how much risk you’re willing to take on future rate and price movement. If you need to move (job relocation, growing family, lease ending), buying now makes sense even at 6.5% to 7.0% rates, especially if you plan to hold the home long term and refinance when rates drop. Locking in a home you can afford today removes timing risk and lets you build equity while you wait for refinancing opportunities. If your timeline is flexible and you can comfortably defer a purchase, waiting might pay off if rates fall in late 2025, but you’ll face more competition, faster sales, and potentially higher prices when that happens.

Pre-approval gives you 60 to 90 days of negotiating leverage, signaling to sellers that you’re serious and financially ready. Some lenders offer full upfront underwriting that extends your approval to 120 days, which is useful if you’re searching in a slower market or targeting a specific neighborhood with limited inventory. Prepare your full document set early. Income verification, credit history, asset statements, debt details. So you can move quickly when the right home appears. Compare multiple lenders and loan products to find the best rate and terms. Even a quarter-point difference adds up over 30 years.

Lock vs Float Strategies

Choosing whether to lock your rate or let it float depends on your risk tolerance and rate outlook. Locking early protects you if rates rise before closing, but you miss out if rates fall. Floating keeps your options open but exposes you to upward rate movement. Your lender can model both scenarios and show you the cost difference.

- Lock early if: you believe rates will rise or stay flat, you need payment certainty for budgeting, or you’re in a competitive market where locking removes one variable from your offer.

- Float if: credible forecasts point to near-term rate declines, you have flexibility to absorb a small rate increase, or your lender offers a “float-down” option that lets you capture declines after locking.

- Hybrid approach: some lenders let you lock with a float-down provision, giving you protection against increases and a chance to benefit from decreases (usually with timing limits and fees).

Loan Product Adjustments

Adjustable-rate mortgages (ARMs) start with lower initial rates than 30-year fixed loans, which can improve affordability if you plan to sell or refinance within five to seven years. A 5/1 or 7/1 ARM offers a fixed rate for the first five or seven years, then adjusts annually based on market indexes. If you expect rates to fall in the next few years, an ARM lets you capture lower payments now and refinance into a fixed-rate loan later. First-time homebuyer programs (FHA, USDA, and state-level assistance) often offer lower down payments, reduced mortgage insurance, or rate buydown options that make monthly payments more manageable. Physician loans, bank-statement loans, and DSCR (debt-service coverage ratio) loans serve specific buyer types and can unlock financing when traditional programs don’t fit your income documentation or property type.

Buydown programs let you or the seller pay upfront to reduce your interest rate temporarily. Common structures are 2-1 or 1-0 buydowns that lower your rate for the first one or two years. If you’re stretching your budget, a buydown reduces early payments and gives you time to increase income or refinance. Jumbo loans (amounts above conforming limits, currently $766,550 in most of Georgia) carry slightly higher rates but are necessary for higher-priced Atlanta neighborhoods like Buckhead or Brookhaven.

Preparing documents early (W-2s, pay stubs, tax returns, bank statements, and existing debt details) speeds up pre-approval and underwriting. The faster you move through approval, the more confident you can be when making offers and the less risk you face from rate changes between contract and closing. To see how pre-approval timelines and underwriting work in Atlanta, check out The Atlanta Housing Market Deep Dive.

How Falling or Rising Rates Could Shift Atlanta Neighborhood Opportunities

Rate declines open doors to neighborhoods that were just out of reach at higher rates. When rates drop from 7.0% to 6.0%, your monthly payment shrinks enough to move you from Smyrna or Marietta into Buckhead or Midtown, or from Decatur’s suburbs into walkable Virginia-Highland. Inman Park, with its historic bungalows and proximity to the BeltLine, becomes affordable for first-time buyers when their monthly budget increases by a few hundred dollars. The same dynamic applies in reverse. When rates rise, buyers shift outward to suburban value areas like Alpharetta, Smyrna, and Marietta, where larger homes and lower price-per-square-foot numbers help offset higher borrowing costs.

Falling rates also accelerate gentrification and price appreciation in transitional neighborhoods. Areas on the edge of established markets (East Atlanta, Kirkwood, parts of South Fulton) see faster buyer interest when affordability improves, because investors and first-time buyers view those neighborhoods as the next wave of appreciation. Rising rates slow that process, giving buyers more time to evaluate and negotiate but reducing the speed at which neighborhoods transition from “emerging” to “established.”

Which buyer types benefit most from rate shifts:

- First-time buyers: Rate drops let you afford condos in Virginia-Highland or starter homes in Decatur instead of renting or settling for farther-out suburbs.

- Growing families: Lower rates bring Sandy Springs, Roswell, and Milton (areas with strong schools and more space) back into budget.

- Investors: Falling rates improve cash flow on rental properties and make fix-and-flip financing more attractive, accelerating activity in value-add neighborhoods.

To explore how falling rates reshape Atlanta neighborhood accessibility and buyer competition, see Will Falling Interest Rates Change The Atlanta Housing Market?.

Final Words

in the action, we covered 2024–2025 Atlanta rate projections, how those moves affect monthly payments, and local quirks like low North Metro inventory that can blunt rate shifts.

We explained the key drivers — Fed signals, bond yields, and local supply — and used recent history to set expectations. Then we gave clear next steps: get pre-approval, weigh lock vs float, consider ARMs or buydowns, and watch neighborhood affordability.

Keep an eye on projected atlanta mortgage rate trends and what buyers should expect, plan your budget, and you’ll be ready when the right home shows up.

FAQ

Q: Will mortgage rates go down to 5% in 2027?

A: Mortgage rates reaching 5% in 2027 is possible but depends on Fed policy, inflation, and bond yields; many economists expect easing by late‑2025–2026, though 5% isn’t guaranteed for Atlanta buyers.

Q: What is the real estate outlook for 2026 in Atlanta?

A: The 2026 Atlanta real estate outlook expects modest price stability with possible demand growth if rates ease; low North Metro inventory may keep prices firm, so watch new construction and rental spillover.

Q: What is the 3 3 3 rule in real estate?

A: The 3‑3‑3 rule in real estate is a budgeting shortcut: keep three months’ mortgage reserves, expect roughly 3% of price for transaction/closing costs, and budget about 3% yearly for maintenance.

Q: What is the hardest month to sell a house?

A: The hardest month to sell a house in Atlanta is often December because of holidays and low buyer activity; late fall and winter (November–January) are slowest, while spring usually sells fastest.