{kind=link}

Think FHA loans always save first-time buyers money? Not in Atlanta.

Mortgage insurance (extra monthly insurance) often drives the real monthly and lifetime cost.

Which loan wins depends on your credit, down payment, price, and how long you plan to stay.

Where you shop matters too — Buckhead, Brookhaven, and parts of Decatur can push loan limits and add repair rules.

If you’re using Invest Atlanta down payment help or bidding in a hot Smyrna listing, the right pick looks different.

This guide walks through Atlanta numbers so you can see which loan saves you more.

Quick Comparison for Atlanta First-Time Buyers

FHA loans make sense when your credit score sits between 580 and 680, you’re putting down less than 5%, or your debt to income ratio pushes toward 50%. Conventional loans usually cost less long term if your credit score is 680 or higher, you can put 5% down, and you plan to stay in the home beyond seven years. The headline interest rate tells only part of the story. Mortgage insurance mechanics drive the real monthly and lifetime cost difference.

Atlanta’s 2024 FHA loan limit is $649,750 for most metro counties. The conventional conforming limit sits at $766,550. That gap matters if you’re shopping in Brookhaven, Decatur, or parts of Buckhead where home prices routinely cross $600,000. Most Atlanta first time buyers land between $300,000 and $500,000, so both programs work on paper. But the long term cost spread can reach six figures depending on how long you hold the loan and when mortgage insurance drops off.

Market conditions across Metro Atlanta influence which loan wins. In neighborhoods like Virginia Highland or Edgewood, older homes often fail FHA inspections due to peeling paint, foundation settlement, or missing handrails. Sellers in hot pockets of Smyrna, Alpharetta, and Sandy Springs sometimes reject FHA offers because appraisal repairs slow closing timelines. If you’re competing in a seller’s market, conventional loans carry fewer property condition strings.

Minimum down payment: FHA 3.5% with credit 580+, Conventional 3% with credit 620+

Credit score threshold: FHA accepts 580, Conventional prefers 680+ for best outcomes

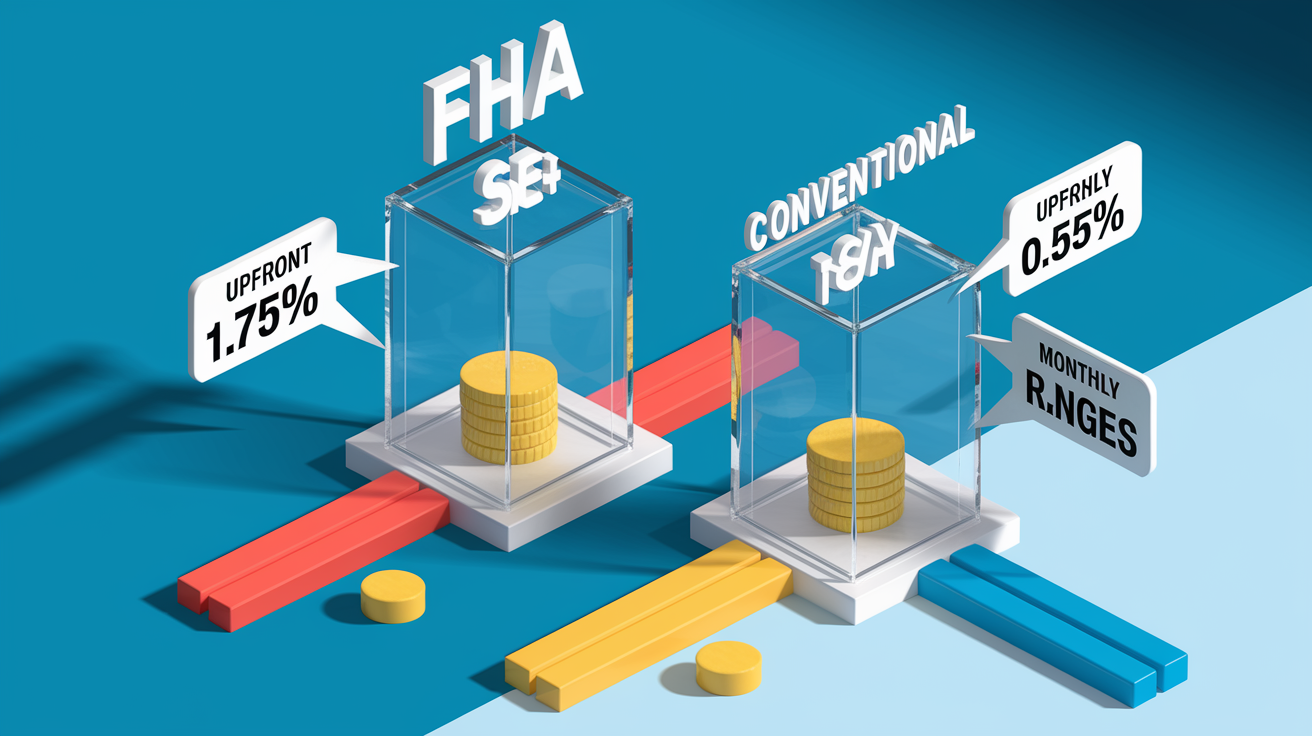

Mortgage insurance: FHA charges upfront MIP (1.75% of loan) plus lifetime monthly MIP. Conventional PMI drops at 20% equity

Atlanta loan limits: FHA $649,750, Conventional conforming $766,550

Eligibility Requirements for FHA and Conventional Loans

FHA sets a minimum credit score of 580 for 3.5% down, but many Atlanta lenders require 600 or higher to approve the file. If your score falls between 500 and 579, FHA still works. You just need 10% down instead of 3.5%. Conventional loans typically require 620 as a floor, and most underwriters want to see 680+ before they’ll approve a 3% or 5% down payment without compensating factors. Below 620, conventional approval becomes nearly impossible unless you bring a co borrower with stronger credit.

Documentation expectations are similar for both programs. Two years of W 2s, one month of pay stubs, two months of bank statements, and tax returns if you’re self employed. FHA underwriters dig into gift funds more carefully but allow broader sources. Friends, employers, and charities can contribute if you document the gift letter correctly. Conventional loans limit gift sources to immediate family or domestic partners. Both programs verify employment within 10 days of closing, so job changes during underwriting can delay or kill approval.

Debt to income ratios create the clearest qualification gap. FHA regularly approves borrowers at 50% DTI, and some files go through at 52% or 53% when compensating factors offset the high ratio. Steady job history, reserves, or lower loan to value all help. Conventional lenders prefer 43% DTI, though some allow 45% with strong credit and reserves. If your monthly debts (student loans, car payments, minimum credit card payments, plus the new mortgage) push your income past 45%, FHA becomes the realistic path.

FHA minimum credit score: 580 (or 500 with 10% down)

Conventional minimum credit score: typically 620, recommended 680+

FHA DTI tolerance: up to 50%, sometimes higher with compensating factors

Conventional DTI preference: 43% or lower, some lenders allow 45%

Gift fund sources: FHA accepts friends, employers, charities. Conventional limits to family or partners.

Cost Breakdown: Upfront and Long-Term Expenses

FHA charges an upfront mortgage insurance premium of 1.75% of the total loan amount. On a $337,750 loan (3.5% down on a $350,000 purchase), that’s $5,911 rolled into the loan balance. You also pay monthly MIP, typically 0.55% annually, which works out to about $155 per month per $100,000 borrowed. Conventional PMI has no upfront fee, but monthly PMI varies widely by credit score. Buyers with 740+ scores might pay 0.30% annually ($125 per month per $100,000), while 680 score borrowers pay closer to 0.70% ($291 per month per $100,000). Closing costs tend to run $3,000 to $6,000 on both programs, though conventional loans sometimes carry slightly higher lender fees due to risk based pricing.

Over five years, FHA’s upfront MIP and higher monthly insurance usually cost $8,000 to $12,000 more than conventional PMI on a $350,000 Atlanta purchase. Over ten years, the gap widens to $20,000 to $25,000 because conventional PMI drops off when you hit 20% equity. That typically happens around year seven with 5% down and 3% annual appreciation. FHA MIP stays for the loan’s life unless you refinance, so a 30 year FHA loan can cost $130,000+ more in insurance alone compared to conventional. Break even happens around year five to seven for most buyers. If you plan to stay longer, conventional saves significantly.

| Cost Category | Upfront Costs | Monthly Costs (Year 1) | Equity-Based Changes |

|---|---|---|---|

| FHA | 1.75% upfront MIP ($5,911 on $337,750 loan) + $3,000–$6,000 closing | ~$302/month MIP (0.55% annual on $337,750) | MIP remains unless refinanced, no automatic drop off |

| Conventional | No upfront PMI + $3,000–$6,500 closing | ~$184/month PMI (0.35% annual on $332,500 at 680 score) | PMI drops at 20% equity (~year 7 with 5% down), payment falls $184/month |

Pros and Cons for Atlanta First-Time Buyers

FHA loans open the door when conventional underwriting shuts you out. You can qualify with a 580 credit score, use 100% gift funds for your down payment and closing costs, and lean on debt to income ratios up to 50%. Atlanta down payment assistance programs (like Invest Atlanta’s 3.5% grant) often require FHA loans, so if you’re stacking DPA to bring your out of pocket cash near zero, FHA becomes the only realistic option. FHA also tends to offer slightly lower interest rates, often 0.125% to 0.25% below conventional, which helps offset some of the insurance cost in the first few years.

Conventional loans cost less over time if you qualify. PMI drops automatically when you reach 20% equity, and you can request removal as early as 22% equity with a new appraisal. If you’re buying in intown Atlanta (Virginia Highland, Kirkwood, Edgewood), conventional appraisals skip the strict property condition checklists that sink FHA deals over peeling paint or missing deck railings. Conventional loans also make your offer more attractive to sellers who’ve been burned by FHA appraisal repairs in the past. That matters in competitive neighborhoods like Smyrna, Alpharetta, and parts of Decatur.

FHA advantages:

Accepts credit scores as low as 580 (500 with 10% down)

Allows debt to income ratios up to 50% or higher with compensating factors

Works with Atlanta DPA programs that require FHA (Invest Atlanta, Atlanta Housing Authority grants)

Typically offers interest rates 0.125% to 0.25% lower than conventional

Conventional advantages:

PMI drops at 20% equity, cutting monthly payment $150 to $300

Fewer property condition restrictions, easier to close on older Atlanta homes

Lower total insurance cost over 10+ years (often $20,000 to $25,000 savings)

Stronger offer appeal in competitive neighborhoods where sellers avoid FHA appraisal repairs

Atlanta Housing Market Context

Atlanta’s median home price sits around $400,000 across the metro, but that number hides wide neighborhood variation. Fulton County intown listings routinely push $500,000 to $700,000, while Gwinnett, Cobb, and parts of South Fulton offer solid inventory between $280,000 and $450,000. FHA buyers usually target the $300,000 to $500,000 range, where 3.5% down ($10,500 to $17,500) plus closing costs stay under $20,000 out of pocket before DPA. Conventional buyers with 5% down need $15,000 to $25,000 cash in the same price tier, which narrows the field unless you’re stacking gifts or savings.

Competition varies by price and location. Listings under $350,000 in Smyrna, Marietta, and Duluth often see multiple offers within 48 hours. Sellers lean toward conventional or cash buyers to avoid appraisal condition delays. FHA appraisals in those areas usually pass without issue because the housing stock is newer and better maintained. Intown, older neighborhoods present the opposite dynamic. Homes need more work, but prices climb faster, so equity builds quicker if you can close the deal. If your income to price ratio pushes above 30% of gross monthly income going to housing, lenders tighten underwriting on both programs. But FHA’s higher DTI tolerance gives you a better shot at approval.

Typical FHA friendly Atlanta areas include newer construction in Brookhaven, Sandy Springs, Alpharetta, and Peachtree Corners. Properties built after 2000 with minimal deferred maintenance. Conventional loans dominate intown markets like Virginia Highland, Candler Park, and East Atlanta because older homes often fail FHA’s paint, foundation, and safety checklists. Condos in Midtown, West Midtown, and Buckhead present another wrinkle. Many HOAs aren’t FHA approved due to owner occupancy ratios or reserve requirements, so conventional becomes the only path.

Long-Term Financial Implications

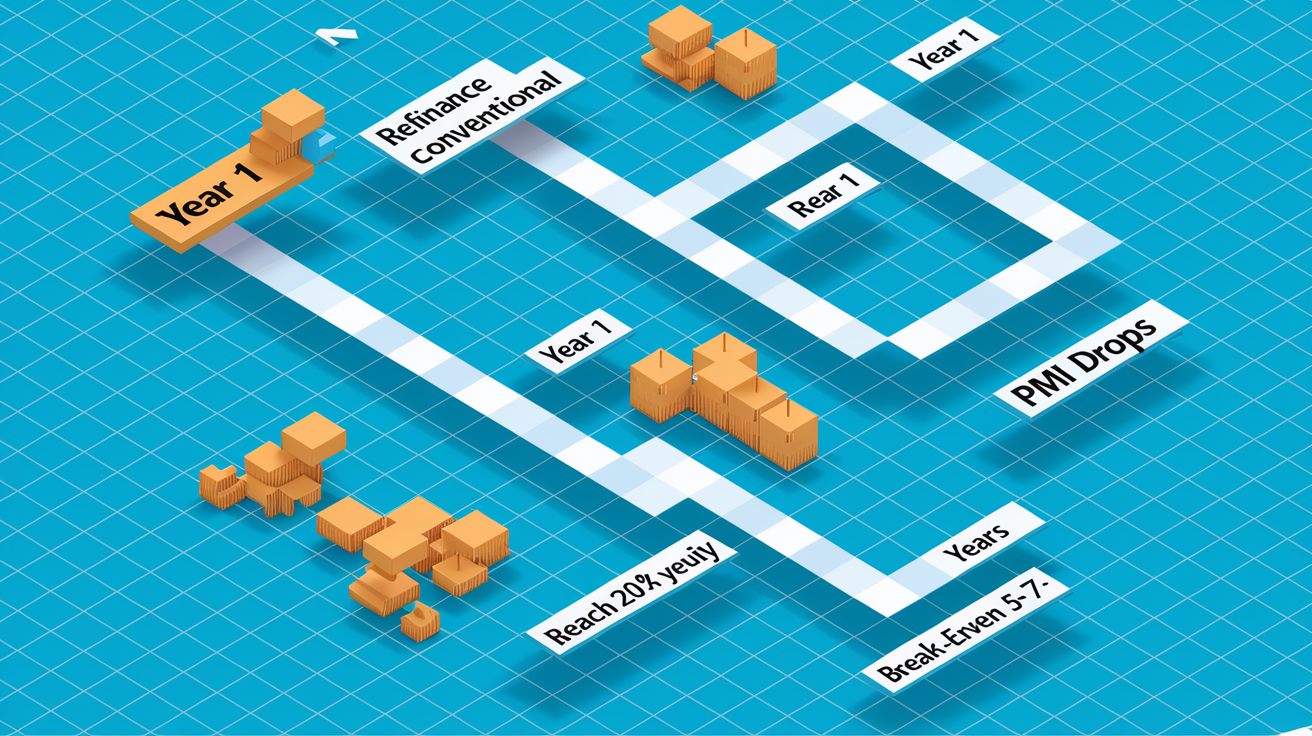

Most FHA buyers refinance to conventional within three to five years once credit improves and home equity crosses 20%. A typical scenario: you bought in 2023 with FHA at 6.0%, credit score 620, and 3.5% down. By 2026, your score climbed to 700, the home appreciated 9% (3% annually), and your loan to value dropped to 86%. Refinancing to conventional at 6.0% eliminates the $302 monthly MIP, cutting your payment from $2,850 to $2,476. A $374 per month savings. Refinance costs run $4,000 to $6,000, so break even happens in 11 to 16 months, and you save $4,488 annually after that.

Equity growth drives refinance timing. With 5% down on a $350,000 home appreciating 3% per year, you hit 20% equity around year six or seven. With 3.5% down, it takes closer to eight or nine years unless appreciation accelerates or you make extra principal payments. Once PMI or MIP drops, your effective monthly housing cost falls 6% to 10%, freeing up cash for savings, debt payoff, or home improvements. If you never refinance an FHA loan, you’ll pay MIP for 30 years. On a $337,750 loan at 0.55% annually, that’s roughly $108,000 in insurance over the loan’s life.

Long term decision factors you should track:

Refinance timeline. Plan to refinance FHA to conventional when credit reaches 680+ and loan to value drops to 80% or lower (typically 2 to 4 years with appreciation and payments).

Equity accumulation. Calculate time to 20% equity using your down payment, expected appreciation (historically 3% to 4% in Metro Atlanta), and principal paydown (first five years pay mostly interest).

PMI removal math. Conventional PMI drops automatically at 78% LTV or by request at 80% LTV with a new appraisal. Track your loan balance and home value annually.

Rate environment. If rates drop 0.75% or more after your purchase, refinancing can eliminate insurance and lower your rate, compounding monthly savings to $400 to $600.

Actionable Tools and Next Steps for Atlanta Buyers

Run both FHA and conventional quotes through a mortgage calculator that breaks out principal, interest, taxes, insurance, and mortgage insurance separately. Plug in your actual credit score, down payment amount, and estimated interest rate. Don’t use national averages. Compare the monthly payment for months 1 through 84 (years one through seven), then compare again after conventional PMI drops off. Most buyers discover FHA costs $100 to $150 more per month early on, then $250 to $350 more after year seven when conventional PMI disappears.

Lender preapproval matters more in Metro Atlanta than in slower markets. Sellers routinely receive multiple offers on homes under $450,000, and a preapproval letter from a local lender (not an online only shop) signals you’re a serious buyer who can close on time. Ask your lender to run both FHA and conventional scenarios, show you 10 year total cost comparisons, and explain exactly when PMI or MIP drops off. If they push FHA without showing long term numbers or skip the conventional quote entirely, that’s a red flag.

Use a total cost calculator that includes upfront MIP, monthly insurance, and equity growth assumptions. Compare 5 year, 10 year, and 30 year totals for both programs.

Get preapproved by an Atlanta lender who works both FHA and conventional products, knows local condo approval lists, and understands intown inspection issues.

Compare at least three lenders. One large bank, one credit union, and one independent mortgage broker. Rate and fee differences often exceed $2,000 over the first year.

Final Words

You’ve just seen a side‑by‑side of FHA and conventional: who they help, Atlanta loan limits, upfront and ongoing costs, and the long‑term tradeoffs.

Next steps are simple: run the numbers with a mortgage calculator, get a lender preapproval, and check how competitive the neighborhood is at your price. If your credit’s lower, FHA often helps. If you can hit higher scores, conventional can save money later.

Use this fha vs conventional loans for atlanta first-time buyers guide to choose with confidence. You’ve got this.

FAQ

Q: Which loan is better for Atlanta first-time buyers: FHA or conventional?

A: Which loan is better for Atlanta first-time buyers depends: FHA fits buyers with lower credit or small down payments, while conventional usually saves money long term if you have stronger credit and a larger down payment.

Q: What are Atlanta-specific loan limits for FHA and conventional?

A: What are Atlanta-specific loan limits: Atlanta’s 2024 FHA loan limit is $649,750 and the conforming conventional limit is $766,550, which affects whether a purchase needs a standard or jumbo mortgage in Metro Atlanta.

Q: How much down payment is required for FHA vs conventional?

A: How much down payment is required: FHA accepts as little as 3.5% with a 580 credit score, while some conventional programs allow 3% but typically expect higher credit scores and stronger cash reserves.

Q: How do mortgage insurance rules differ between FHA and conventional?

A: How mortgage insurance rules differ: FHA charges a 1.75% upfront MIP plus monthly MIP often for the loan’s life, while conventional PMI varies by credit and can be removed once you reach about 20% equity.

Q: What minimum credit scores do FHA and conventional loans require?

A: What minimum credit scores do FHA and conventional loans require: FHA allows 580 for a 3.5% down payment (lower with bigger down), while conventional loans usually require about 620+ for standard approval and better rates.

Q: How does debt-to-income (DTI) affect FHA and conventional approvals?

A: How DTI affects approvals: DTI affects approval because FHA is generally more flexible with higher debt-to-income ratios, while conventional lenders are stricter and may charge worse pricing or deny high-DTI applicants.

Q: Which Atlanta neighborhoods tend to be FHA-friendly versus conventional-friendly?

A: Which neighborhoods tend to be FHA- vs conventional-friendly: FHA buyers often target homes under $600k in OTP and older intown areas; conventional buyers compete in higher-priced Buckhead, Midtown, and fast-appreciating neighborhoods.

Q: Can I refinance an FHA loan to a conventional loan to remove mortgage insurance?

A: Can you refinance FHA to conventional: You can refinance from FHA to conventional once you have enough equity—generally about 20%—which allows removal of FHA MIP and often lowers your monthly payment.

Q: How do upfront and long-term costs compare between FHA and conventional over 5–10 years?

A: How upfront and long-term costs compare: FHA has a 1.75% UFMIP plus ongoing MIP, often costing more long term; conventional may cost less over 5–10 years once PMI ends after reaching sufficient equity.

Q: What practical next steps should Atlanta first-time buyers take?

A: What next steps should Atlanta first-time buyers take: Get lender preapproval, use mortgage calculators to compare total costs, and meet a few local lenders who know Atlanta limits and neighborhood competition before you bid.