{kind=link}

Think a down payment is the only thing keeping you out of a Fulton County house?

It doesn’t have to be.

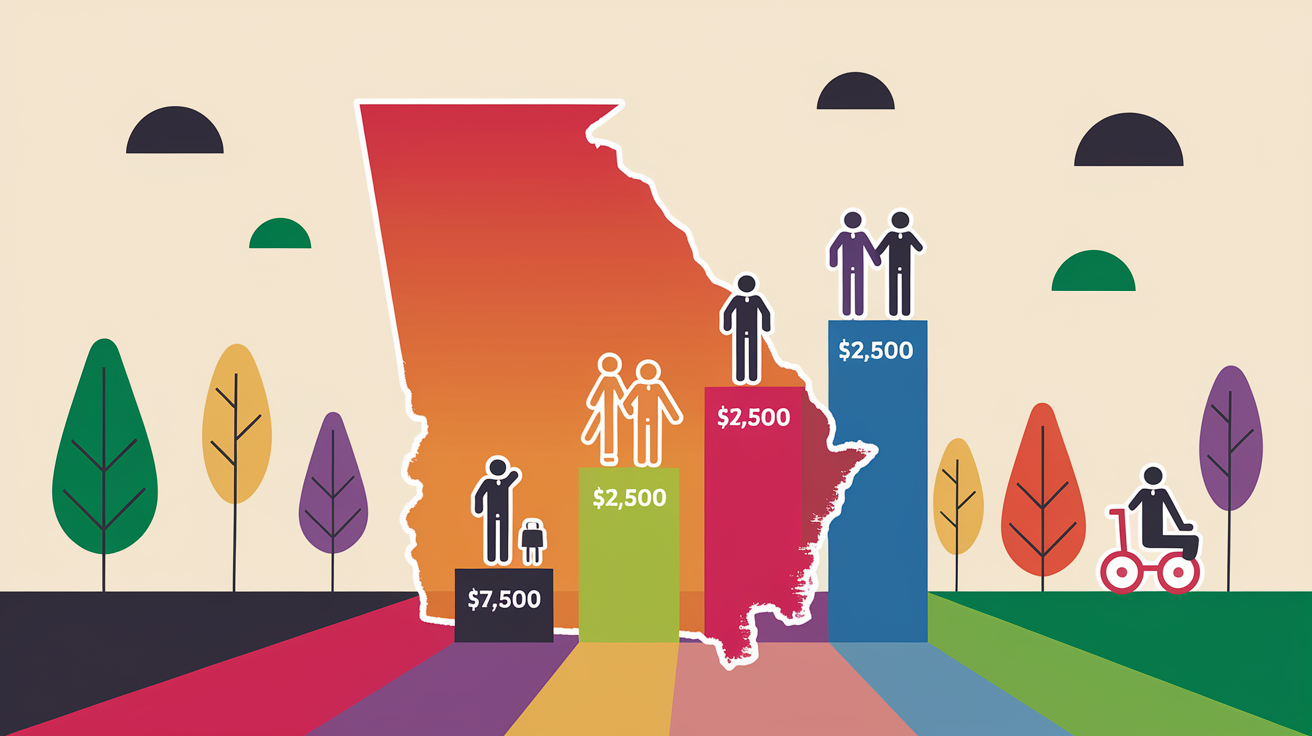

Fulton County and Atlanta offer five main down payment help programs, from about $7,500 up to $30,000.

Some cover the whole county. Some only work inside Atlanta city limits or in unincorporated pockets.

Most aid is a deferred second loan that forgives over time if you live in the home.

This post breaks down each program, who qualifies, and how to pick the one that actually fits your situation.

Overview of Fulton County Down Payment Assistance Options

First-time homebuyers in Fulton County have five major down payment assistance programs to choose from. Each one has different funding levels, eligibility rules, and service areas. Some cover the entire county. Others only work if you’re buying inside Atlanta city limits or specific unincorporated zones. Most assistance comes as a deferred second mortgage that gets forgiven after you live in the home for a set number of years.

The programs range from $7,500 to $30,000 in assistance. Each has its own income caps, credit requirements, and homebuyer education rules. Some are run by Fulton County. Some by the City of Atlanta or Invest Atlanta. One is statewide through the Georgia Department of Community Affairs. You can combine certain programs with others, but geography and income limits will determine which ones you actually qualify for.

| Program Name | Maximum Assistance | Eligibility Highlights | Geographic Limits | Loan/Grant Structure |

|---|---|---|---|---|

| Fulton County HOP | Up to $10,000 | Income limits by household size; liquid assets under $5,000 | Fulton County only (outside Atlanta, Sandy Springs, Johns Creek) | Deferred payment second; no payment for up to 6 years while owner-occupied |

| Atlanta Housing DPA | Up to $20,000 (up to $25,000 for public service workers) | Income ≤80% AMI; Georgia resident for six months; first-time buyer or no ownership in last three years | Eligible areas within Atlanta city limits (portions of Fulton County) | Forgivable loan after 10 years of owner occupancy |

| Invest Atlanta HomeFirst | Up to $30,000 | Income caps apply; homebuyer education required; liquid assets up to $25,000 | Inside Atlanta city limits only (Fulton or DeKalb) | Deferred forgivable loan after five years |

| Georgia Dream DPA | $7,500 standard; up to $10,000–$12,500 for special categories | First-time buyer or no ownership in last three years; income limits vary by county | Statewide (all of Fulton County) | DPA loan; terms vary by program variant |

| FHA Zero-Down + Lender DPA | Varies by lender; often 3.5%–5% of sales price | Minimum credit score 600+; income restrictions by program | Statewide availability (Fulton County included) | Second mortgage, some forgivable after 36 on-time payments |

Fulton County HOP Program Details

The Fulton County Home Ownership Program offers up to $10,000 toward closing costs if you’re buying in unincorporated Fulton County. That means properties outside the city limits of Atlanta, Sandy Springs, and Johns Creek. The assistance is structured as a deferred-payment second mortgage. You won’t make payments on it for up to six years as long as you live in the house as your primary residence. No, you can’t rent out the property and keep the deferred benefit.

Income limits get updated every year and depend on how many people live in your household. For a single person, the cap is $40,150. Family of four, it’s $57,350. Larger households can earn up to $75,700 (eight people). Maximum sales price is $225,625, and you must have less than $5,000 in liquid assets. Retirement accounts and 401(k)s don’t count toward that $5,000, which helps if you’ve been saving for a few years.

You’ll need to complete both pre-purchase and post-purchase homebuyer education classes. The property must pass a home inspection that meets program requirements. To start, call (404) 601-4152 and mention down payment assistance, or apply online through the program portal. Loan approval is subject to credit review, and the program works with lenders that can originate FHA, VA, and USDA loans. Confirm your lender is program-eligible before you get too far into the process.

Atlanta Housing Down Payment Assistance (Eligible Parts of Fulton County)

Atlanta Housing provides up to $20,000 in assistance for eligible first-time buyers purchasing homes inside Atlanta city limits, which includes the Atlanta portions of Fulton County. Public safety officers, healthcare workers, educators, active military, and veterans can qualify for up to $25,000. The DPA is completely forgiven after you live in the home as your primary resident for 10 consecutive years. If you move or sell before that, you’ll likely have to repay some or all of the assistance. Confirm repayment terms with the program before you close.

To qualify, your household income must be at or below 80% of the area median income for the Atlanta metro. You must have been a documented Georgia resident for at least six months. You also need to meet the first-time homebuyer definition: either you’ve never owned a home, or you haven’t owned one in the past three years. You can combine this DPA with other homebuyer programs if the rules allow it. That can help stack funding if you’re trying to cover both down payment and closing costs.

Atlanta Housing’s geographic boundary matters. If the property address falls outside Atlanta city limits, this program won’t apply, even if it’s still in Fulton County. Check the city boundary map or ask your real estate agent to confirm before you tour. The application process includes HUD-approved homebuyer counseling, income documentation, and lender pre-approval from a participating mortgage company.

Invest Atlanta HomeFirst and Other DPA Programs

Invest Atlanta’s HomeFirst program offers up to $30,000 in down payment assistance. One of the highest amounts available in the metro. The catch is geography: you must purchase a home inside Atlanta city limits, in either the Fulton County or DeKalb County portions of the city. The assistance is structured as a deferred forgivable loan, which means it’s forgiven after five years of homeownership if you stay in the home as your primary residence.

Income caps vary depending on household size and are tied to area median income thresholds. Buyers are required to complete homebuyer education, and there’s a $1,200 participant fee that covers the coursework. You can have up to $25,000 in liquid assets, which is more flexible than some other programs. Eligible properties include single-family homes, condos, townhomes, and 2–4 unit apartments, with a maximum purchase price of $375,000. You’ll need to work with an AHRA (ATL Home Renovation Advantage) participating lender and a participating closing attorney. Ask your loan officer early if they’re approved.

Invest Atlanta also runs smaller assistance programs and renovation-focused options. The ATL Home Renovation Advantage provides up to $10,000 in DPA if you’re using a 30-year fixed FHA, VA, or conventional renovation mortgage. Useful if you’re buying a fixer-upper inside the city. Same five-year forgiveness rule applies.

Georgia Dream Statewide Down Payment Assistance

Georgia Dream is a statewide program managed by the Georgia Department of Community Affairs. It’s available to buyers purchasing anywhere in Fulton County. Standard assistance is $7,500, but educators, public protectors (police, fire, EMTs), healthcare workers, and buyers with family members living with a disability can qualify for up to $10,000–$12,500. You must be a first-time homebuyer, or if you’ve owned before, you can’t have owned a home in the last three years. Some repeat buyers in targeted areas may qualify under exceptions. Confirm that with a Georgia Dream participating lender.

Income limits vary by county and household size. Check the current caps for Fulton County before you apply. You’ll need credit approval for a 30-year fixed-rate mortgage (FHA, USDA-RD, VA, or conventional) from a Georgia Dream participating lender. Not every lender is approved, so ask upfront. The program structures DPA as a loan, and terms depend on which variant of Georgia Dream you use. Some versions include a Mortgage Credit Certificate (MCC) option, which gives you a federal tax credit that can lower your annual tax bill and help you qualify for a slightly higher loan amount.

Georgia Dream is one of the easier programs to access because it’s statewide and works with a large network of lenders. Same-day pre-approvals are common, according to some program materials. If you’re ready to move quickly, this can be a good fallback option even if you don’t land a city or county-specific program.

FHA‑Based Zero‑Down and Lender‑Provided Assistance Options

Some mortgage lenders in Georgia offer FHA-supported financing that gets you to 100% financing when you combine a low-down-payment FHA loan (3.5%) with a second mortgage that covers the rest. One example is the Chenoa Fund, which provides 3.5% or 5% of the sales price or appraised value as DPA. Minimum credit score is usually 600 or higher. The DPA second mortgage can be forgivable after 36 consecutive on-time payments on your first mortgage. That forgivable option is only available on certain loan servicing setups, so ask your lender which structure you’re getting.

These lender-provided options are available across Fulton County and don’t have the same strict geographic boundaries as city or county programs. Income restrictions and credit requirements vary by lender and product, so shop around. Some programs allow manufactured homes with exceptions, and most require the property to be your primary residence. Eligible property types include 1–2 unit homes, condos (FHA-approved or Single Unit Approval), and PUDs.

Unified Comparison Table: Fulton County Buyer Eligibility & Requirements

| Program | Income Cap | Geography | Education Required | Forgivable/Repayable | Maximum Assistance |

|---|---|---|---|---|---|

| Fulton County HOP | $40,150 (1 person) to $75,700 (8 people) | Fulton County (outside Atlanta, Sandy Springs, Johns Creek) | Yes, pre- and post-purchase | Deferred for up to 6 years while owner-occupied; repayment terms after that period not specified | $10,000 |

| Atlanta Housing DPA | ≤80% AMI | Inside Atlanta city limits (portions of Fulton County) | Yes, HUD-approved counseling | Forgivable after 10 years of owner occupancy | $20,000 (up to $25,000 for public service workers) |

| Invest Atlanta HomeFirst | Varies by household size and AMI | Inside Atlanta city limits (Fulton or DeKalb) | Yes, $1,200 participant fee | Forgivable after 5 years of homeownership | $30,000 |

| Georgia Dream DPA | Varies by county and household size | Statewide (all of Fulton County) | Varies by lender and program variant | DPA loan; terms vary | $7,500–$12,500 |

| FHA Zero-Down + Lender DPA | Income restrictions vary by lender/product | Statewide (Fulton County included) | Not always required; confirm with lender | Some forgivable after 36 on-time payments | 3.5%–5% of sales price or appraised value |

Final Words

You saw the main Fulton County options in action: HOP, Atlanta Housing, Invest Atlanta HomeFirst, Georgia Dream, and FHA/lender choices. The post laid out what each program offers, who qualifies, and whether funds are forgivable or repaid.

Next steps are clear: check income and geography limits, finish required homebuyer education, and talk to a lender about pairing programs with your mortgage.

If you’re ready to move, fulton county down payment assistance for first-time buyers can really close the gap. Get pre-approved and you’ll be in a stronger spot to make an offer.

FAQ

Q: What is the $50,000 down payment assistance in Georgia?

A: The $50,000 down payment assistance in Georgia refers to larger local or developer DPA packages, but most Fulton programs top at $30,000; check specific program rules and eligibility before assuming $50k is available.

Q: What is the Fulton County Downpayment Assistance Program?

A: The Fulton County Downpayment Assistance Program is the HOP, offering up to $10,000 for eligible buyers buying outside Atlanta city limits, with income caps, required homebuyer education, and deferred forgivable loans after occupancy.

Q: What is the Atlanta grant for first-time home buyers?

A: The Atlanta grant for first-time home buyers covers programs like Atlanta Housing’s DPA (up to $20,000) and Invest Atlanta’s HomeFirst (up to $30,000); both require HUD-approved counseling and apply only inside city limits.

Q: What’s the minimum down payment for a $300,000 house?

A: The minimum down payment for a $300,000 house depends on loan type: Conventional 3% = $9,000; FHA 3.5% = $10,500; VA/USDA can be 0% if eligible; DPA can also cover your down payment.